Pol�tica Cambiaria y Monetaria.

Lunes 1 de septiembre de 2014

�Leaning against the wind�: exchange rate intervention in emerging markets works

Fuente:

Vox

Autor:

Christian Daude, Eduardo Levy Yeyati

The economic debate has typically downplayed the exchange rate-smoothing nature of central bank foreign exchange intervention, attributing it to precautionary or prudential motives, or to the goal of keeping the exchange rate undervalued for mercantilist reasons. There is plenty of evidence, however, indicating that intervention is primarily geared to limiting what policymakers may see as unwarranted (and possibly harmful) deviations from equilibrium levels (BIS 2005, 2013) – intervention correlates negatively with exchange rate pressure and is often complemented with capital restrictions and taxes that could only make any precautionary reserve build-up more costly.1

In a new paper (Daude et al. 2014) we document the prevalence of this ‘leaning against the wind’ exchange rate intervention in emerging economies; in addition, we show that intervention indeed mitigates real exchange rate (RER) volatility as expected.

Because of the two-way causality between intervention and exchange rate variations – central banks purchase (sell) dollars to partially offset appreciations (depreciations) – the literature has not been successful at documenting a significant and systematic link between interventions and their desired effect on the exchange rate, which typically prove not to be significant and, sometimes, show up with the ‘wrong’ sign. Moreover, not all interventions are exchange rate-driven – a large body of research has shown that intervention may instead be due to reserve restocking after a currency crisis (Aizenmann and Lee 2007), or to precautionary reserve stock-building (and un-building) to ensure a reserve coverage of broad monetary aggregates.

In particular, Obstfeld et al. (2010) argue that the intervention objective is to keep the reserve stock stable relative to the broad monetary aggregate that typically runs against reserves in a currency attack. We build on this literature to compute a central bank intervention measure that filters out possible precautionary causes and minimises the endogeneity bias. We follow Levy Yeyati et al. (2013) and use a ‘strict’ intervention proxy defined as the change in the reserves-to-M2 ratio (where reserves are computed as the central bank’s net foreign asset position excluding gold). We use a two-stage approach. First we estimate an equilibrium real exchange rate (ERER) and then we analyse the effectiveness of interventions in an error correction model.2

A few aspects stand out from our estimates of ERERs:

ERERs display a larger volatility in emerging than in advanced economies (particularly, in Latin American and the Caribbean).

Despite heavy intervention, the boom and bust cycle around the 2008 financial collapse was associated with important deviations of the RER from the (predicted) ERER – a finding that a priori justifies the ‘leaning against the wind’ policy chosen by many countries in the region.

ERERs may differ significantly depending on whether they are estimated based on current (short-run) or trend (medium-run) fundamentals –again, a motive to offset temporary capital flows or commodity bonanzas through intervention (Figure 1).

Figure 1. Average difference between equilibrium real exchange rate estimates at current vs. trend values by regions

In the error correction estimation, where we evaluate whether and to what extent central bank intervention effectively leads to changes in the RER in the expected direction. As it turns out, it does. A 1% increase in our intervention variable is associated with a 0.18% depreciation. Indeed, in line with the attenuation bias mentioned above, once the intervention variable is instrumented, its point estimate increases almost three times. Moreover, it reveals an asymmetry – a significantly larger effect of purchases (almost twice as high) relative to sales, suggesting that intervention is more effective in containing appreciation pressures.3�The results are robust to alternative econometric techniques and sample cuts; in particular, the effectiveness of intervention is similar across Latin American, Asian, and other emerging markets.

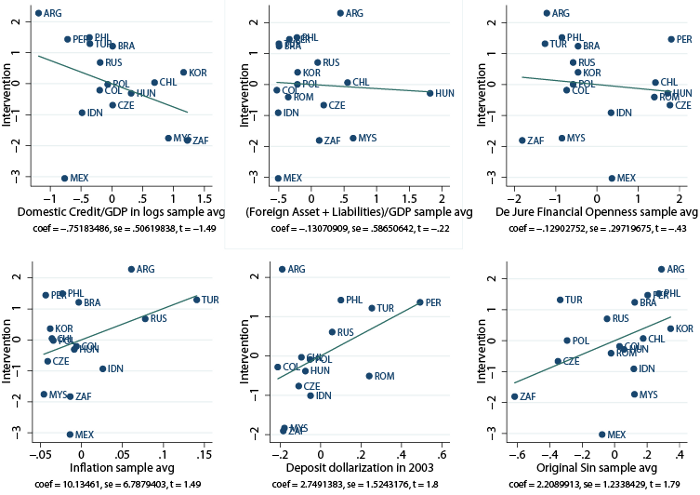

A number of domestic characteristics influence the intensity of the effect and shed preliminary light on the channels through which intervention may affect the exchange rate (Figure 2). For example, the effectiveness of intervention declines with inflation and with the degree of financial dollarisation (as measured by the initial deposit dollarisation ratio). This is a priori consistent with the premise that higher (and more volatile) levels of inflation detract from the central bank’s credibility and, as a result, from the signalling channel of central bank interventions; it is also in line with the fact that, in financially dollarised economies, greater substitutability between local and foreign currency assets may weaken the portfolio channel.4�In addition, interventions are more effective in countries with more developed financial markets – a result that may be capturing the fact that local market development is generally associated with a greater demand for local currency and lower currency substitution. By contrast, intervention effectiveness does not appear to be correlated with de jure and de facto measures of financial openness.

Figure 2. Correlations between intervention effectiveness and financial market characteristics

In sum, this evidence supports the view that central bank intervention can alter the exchange rate in the short run – a premise that, while accepted by most practitioners, had so far received only partial confirmation in the empirical academic literature.

References

Adler, G and C E Tovar (2011), “Foreign Exchange Intervention: A Shield Against Appreciation Winds?”, IMF Working Paper WP/11/165.�

Aizenman, J and J Lee (2007), “International Reserves: Precautionary Versus Mercantilist Views, Theory and Evidence”,�Open Economies Review, 18(2): 191–214.

BIS (Bank for International Settlements) (2005), “Foreign Exchange Market Intervention in Emerging Markets: Motives, Techniques, and Implications”, BIS Paper 24.�

BIS (2013), “Market volatility and foreign exchange intervention in EMEs: what has changed?”, BIS Paper 73.�

Calvo, G A and C M Reinhart (2002), “Fear of Floating”,�Quarterly Journal of Economics, 117(2): 379–408.

Daude, C, E Levy Yeyati, and A Nagengast (2014), “On the effectiveness of exchange rate intervention in emerging markets”, OECD Development Centre Working Paper 324.

Levy Yeyati, E (2010), “What drives reserve accumulation (and at what cost)?”, VoxEU.org, 30 September.�

Levy Yeyati, E (2006), “Financial dollarization: evaluating the consequences”,�Economic Policy, 21(45): 61–118.

Levy Yeyati E, F Sturzenegger, and P A Gl�zmann (2013), “Fear of Appreciation,”�Journal of Development Economics, 101: 233–247.

Levy Yeyati, E and F Sturzenegger (2010), “Monetary and exchange rate policies”, Chapter 64 in D Rodrik and M Rosenzweig (eds.),�Handbook of Development Economics, Vol 5: 4215–4281.

Obstfeld, M, J C Shambaugh, and A M Taylor (2010), “Financial Stability, the Trilemma, and International Reserves”,�American Economic Journal: Macroeconomics, 2: 57–94.

Sarno, L and M P Taylor (2001), “Official Intervention in the Foreign Exchange Market: Is It Effective and, If So, How Does It Work?”,�Journal of Economic Literature, 39(3): 839–868.

Footnotes

1�See, among others, Levy Yeyati (2010) and Adler and Tovar (2011). Sarno and Taylor (2001) provide an early survey for advanced countries, and more recently Levy Yeyati and Sturzenegger (2010) provide a review with a focus on developing economies.

2�We estimate the ERER as a function of standard fundamentals (productivity, commodity terms of trade, net foreign assets, trade openness, and government consumption) using a dynamic ordinary least squares estimation on a balanced panel of emerging and advanced economies at quarterly frequency. From this, we obtain a measure of RER misalignment. Next, we run a short-run error correction model of real exchange rate changes as a function of the exchange rate misalignment and the change in the fundamentals, augmented by additional non-fundamental financial variables that may introduce short-term deviations. To this equation we add our measure of exchange rate intervention to tests its effect on the RER. To correct for the potential endogeneity bias (the fact that intervention may respond to changes in the exchange rate as much as the other way around), we instrument intervention with the change in the M2-to-GDP ratio.

3�Note also that changes in global risk aversion – proxied by changes in the VIX index of implied volatility in options on the S&P500 – have a negative and significant effect on the RER, in line with the anecdotal evidence that global risk-off events are associated with emerging currency sell-offs. Also, the error correction term is always negative and significant at 1%, and implies a half-life between 23 and 27 months – close to the 2.5 years often found in earlier studies.

4�Note that, to the extent that the pass-through from the exchange rate changes to price changes increases with the initial level of inflation, financial dollarisation (which reflects the pass-through) and inflation may be correlated (Levy Yeyati 2006).

�